An Overview of the New Tax Plan for 2018

| Posted by: James Soller | No Comments

With the passage of the Tax Cuts and Jobs Act (TCJA) in December, there are some significant changes that taxpayers need to be aware of as we move into 2018. In reality, this is really more of an overhaul of the previous tax system that you have likely gotten used to over the past 8 years. Fortunately, with a little research, planning and consulting with our experienced tax experts, you can properly prepare yourself for these changes. From tax rate schedules to health care accounts, standard deductions and retirement contribution accounts, there are changes in the new plan that you as the taxpayer need to understand. Additionally, there are several provisions that have been eliminated.

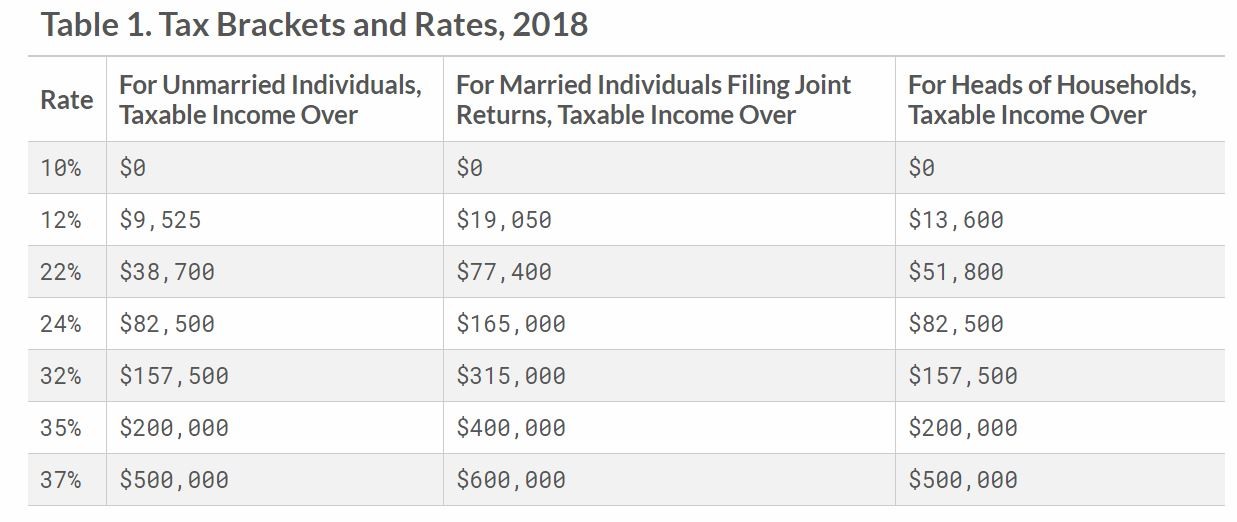

While this article is intended to provide a general overview of the new tax policy, we will be publishing a series of blog posts in the coming weeks that further investigates more specific parts of it. The first significant change is the restructuring of the tax brackets into new tax rate schedules. The number of brackets in the tax schedule remains the same at seven. However, as displayed in the chart below, the rates have decreased for all brackets. They are: 10%, 12%, 22%, 24%, 32%, 35% and 37%. It is also important to remember that these rates won’t expire until 2025 and they could be extended beyond that by Congress.

Some notable provisions under the new tax plan

In addition to the reorganization of tax brackets, there are other significant changes to consider. On the other hand, some common provisions remain relatively unaffected. A few of these have been highlighted below.

The Standard Deduction

Besides the the new tax rates, the other big adjustment that is the topic of many conversations is the jump in standard deductions. In 2018, the standard deduction increases to $12,000 for individuals (an increase from $6,350 in 2017) and to $24,000 for married couples (an increase from $12,700 in 2017). Below is a full breakdown of standard deductions.

- Married Filing Jointly/Surviving Spouse: $24,000

- Heads of Households: $18,000

- Single: $12,000

- Married Filing Separately: $12,000

Earned Income Tax

The earned income credit is one provision that won’t change much under the new tax law. The maximum Earned Income Tax Credit in 2018 for single and joint filers is $520, if the filer has no children. For one child, the credit is $3,468, $5,728 for two children, and $6,444 for three or more children. These numbers are only slightly more compared to 2017. The maximum amount available for joint filers with 3 or more qualifying children in 2017 was $6,318.

Child Tax Credit

Under the new tax rules, the child tax credit increases from $1,000 in 2017 to $2,000 in 2018. This amount is set until at least 2025.

Popular deductions that are eliminated in 2018 under the new tax plan

Moving Expenses

Moving cost have become a popular tax write-off in recent years. Unfortunately for many taxpayers, this is eliminated under the new plan. In 2015 alone, an estimated 1.1 million taxpayers took advantage of this deduction. While many taxpayers will be disappointed to see this disappear, the large increase in the standard deduction should be enough to compensate for its loss.

State and local property taxes

Another hot topic concerning the new tax law are state and local property taxes. The new tax plan hurts taxpayers in parts of the East Coast and California, where housing cost and property taxes are high. Under the new plan, homeowners can only deduct up to $10,000 in property tax whereas the deduction was unlimited in the past. Although the increase in the Standard Deduction will help to offset this for homeowners in high-income states, it certainly will not be enough.

Alimony

Getting divorced may become pricier for some individuals under the new tax plan. Under the new plan, alimony payments are no longer deductible. However, this only applies to those that get divorced after December 31st of 2018. Those currently paying alimony will not be affected.

Planning For New Tax Regulations in 2018?

It’s 2018 and a new tax law has been passed. Now is the time to plan and take a proactive approach in anticipation for the new tax regulations. Get in touch with us, so that we can help you keep more of your money.

If you found this informative, share it with your friends! Click on the icon to the left.